Sole Trader vs Limited Company: Which Structure is Right for You in 2026?

What if the tax savings you are chasing are being swallowed by the very structure meant to protect them? If you are currently weighing up the choice between a sole trader vs limited company setup, you are likely feeling the pressure of the new Making Tax Digital (MTD) for ITSA rules that took effect on 6 April 2026. We know that the anxiety of personal liability and the confusion over salary versus dividends can feel overwhelming, especially with HMRC reporting an 18.5% tax gap amongst self-assessment businesses. You deserve to focus solely on your goals without the constant fear of administrative “red tape” or unexpected penalties.

This guide provides a clear path through the legal and financial maze to ensure your business can truly flourish. We will identify the specific £50,000 profit tipping point where switching structures becomes most beneficial and explain how to navigate the 19% Small Profits Rate whilst staying completely compliant. By the end, you will have a tax-efficient plan to pay yourself and the reassurance that your personal assets are shielded from business debts.

Key Takeaways

- Understand the fundamental legal distinctions between structures to ensure your personal assets remain shielded from business liabilities and debt.

- Identify the specific profit thresholds where the choice of sole trader vs limited company impacts your overall tax efficiency in the 2026/27 tax year.

- Prepare for the administrative shift brought by Making Tax Digital (MTD) for ITSA, which introduces new digital record-keeping requirements from April 2026.

- Evaluate the “Tax vs Task” balance to determine if the potential tax savings of a company structure outweigh the increased filing responsibilities and Companies House fees.

- Learn how a “beyond the books” approach to your accounts provides the calm competence needed to manage HMRC compliance whilst you focus on your business goals.

Understanding the Legal Foundations: Sole Trader vs Limited Company

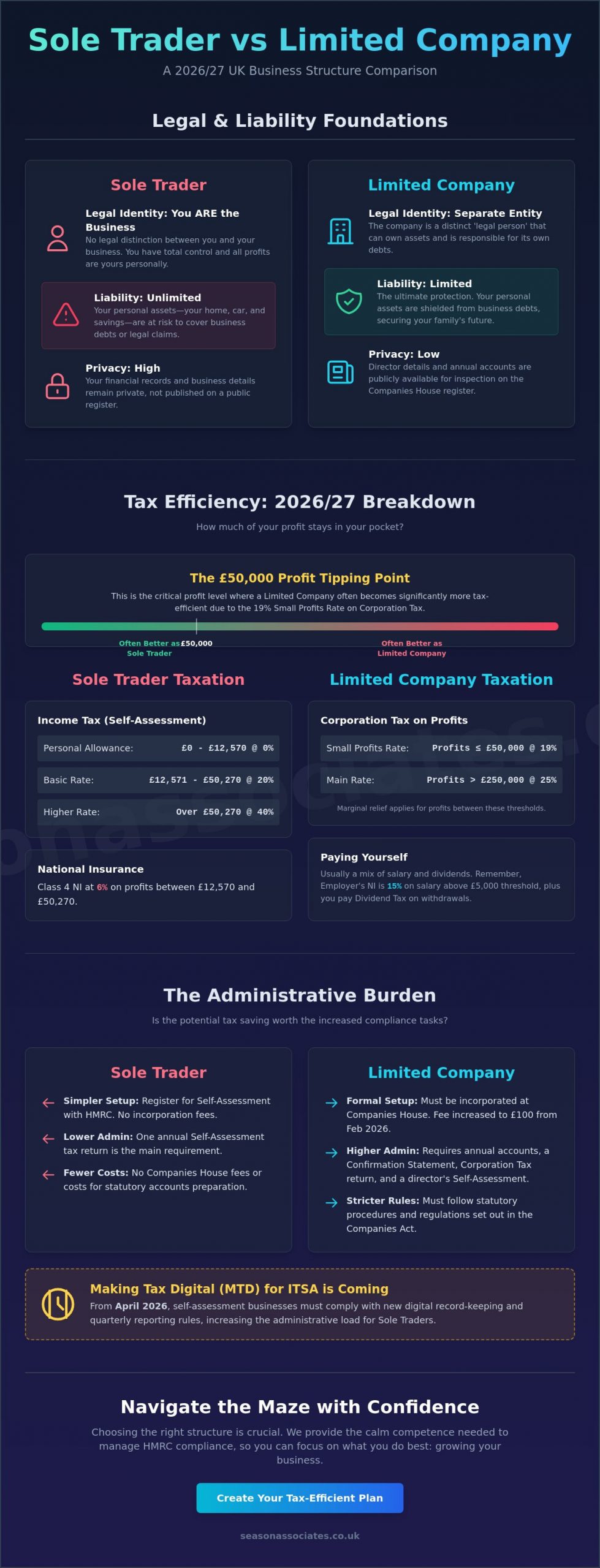

Are you just starting out or has your freelance venture reached a new peak? Choosing between a sole trader vs limited company structure is the first major hurdle for any entrepreneur in 2026. A sole trader is essentially the simplest form of business ownership. Legally, you and the business are one and the same entity. This means you have total control, but you also carry all the responsibility. To gain a deeper perspective on the historical and global context, Understanding Sole Proprietorship provides a neutral overview of how this structure functions across different jurisdictions. Conversely, a limited company is a separate legal person in its own right. It can own property, enter into contracts, and is responsible for its own debts. While a sole trader offers agile simplicity, a limited company provides a level of prestige that often appeals to larger corporate clients.

To better understand this concept, watch this helpful video:

The Legal Identity and Ownership

In a sole trader setup, you own every piece of equipment and every penny of profit personally. A limited company owns its assets on behalf of its shareholders. If you are the sole director, you still make the decisions, but you must follow statutory procedures. It’s a trade-off; companies face stricter public disclosure requirements. Your annual accounts and director details will be visible on the Companies House public register, whereas a sole trader’s financial records remain private. Starting a company also involves higher initial costs, such as the £100 digital incorporation fee introduced on 1 February 2026, which reflects the increased administrative framework required for this structure.

Personal Liability: Protecting Your Home and Assets

Limited liability is the legal protection of your personal assets from business debts or legal claims. This distinction is vital for risk management. If a sole trader is sued or enters debt, their personal home, car, and savings are at risk because there is no legal firewall between the individual and the business. In industries like construction or high-risk consulting, where professional indemnity claims can be substantial, the limited company shield is often a non-negotiable requirement for peace of mind. While the sole trader model is often easier to organise, the protection offered by a company structure ensures that your family’s security isn’t tied to the volatile fortunes of the marketplace.

Tax Efficiency in 2026: Corporation Tax vs Self-Assessment

How much of your hard-earned profit actually stays in your pocket? This is the central question when weighing up a sole trader vs limited company structure. For the 2026/27 tax year, sole traders face a frozen Personal Allowance of £12,570, with a 20% basic rate on income up to £50,270 and a 40% higher rate beyond that. Limited companies, however, operate under a tiered Corporation Tax system. If your profits are £50,000 or less, you will benefit from the 19% Small Profits Rate. If profits exceed £250,000, the rate jumps to 25%, with marginal relief bridging the gap for those in between. While the sole trader path is supported by official government guidance on setting up as a sole trader, the limited company structure often offers more sophisticated ways to manage your tax exposure.

National Insurance (NI) adds another layer of complexity. Sole traders pay Class 4 NI at 6% on profits between £12,570 and £50,270. In contrast, company directors are subject to Class 1 NI. For 2026/27, employers now pay 15% NI on earnings above the £5,000 secondary threshold. This shift in NI rates means the old strategy of “low salary, high dividends” requires more precise calculation than in previous years. Many entrepreneurs worry about “double taxation,” but this is largely a misunderstanding of the sequence. Your company pays Corporation Tax on its profits first; you then pay Dividend Tax only on the money you choose to take out. If you leave money in the business to reinvest, that second layer of tax doesn’t apply.

Paying Yourself: Salary, Dividends, and Drawings

In a sole trader setup, you simply take “drawings” from the business. There is no formal payroll, and you’re taxed on the total profit regardless of how much you actually spend. Limited company directors have more control but face more “red tape.” You’ll typically take a small salary to utilise your £12,570 Personal Allowance and then extract further profit as dividends. It’s vital to remember the 2026 Dividend Allowance is now just £500. Anything above this is taxed at 10.75% for basic rate payers or 35.75% for higher rate payers. Our team can help you organise a tax-efficient remuneration strategy that balances these different rates.

The 2026 Tipping Point: When Does it Pay to Switch?

The “tipping point” is the profit level where the tax savings of a company outweigh the extra accountancy fees and administrative costs. In 2026, this threshold typically sits amongst the £30,000 to £50,000 profit mark. However, this isn’t a one-size-fits-all figure. A limited company allows you to treat pension contributions as a pre-tax business expense, which can significantly lower your Corporation Tax bill. Finding your personal tipping point requires detailed tax planning to ensure your chosen structure continues to help your business flourish as you grow.

The Administrative Burden: Red Tape and Compliance

Does the thought of “red tape” keep you awake at night? It’s a common anxiety for those debating the sole trader vs limited company path. While the UK government guide to setting up as a sole trader highlights a relatively straightforward entry into business, a limited company demands a more disciplined approach. You aren’t just a business owner; you’re a director with statutory obligations. This includes filing a Confirmation Statement annually and submitting full statutory accounts to Companies House. Since 1 February 2026, the digital confirmation statement fee has risen to £50, making it essential to get your filings right the first time to avoid wasted costs and unnecessary stress.

You must also maintain accurate statutory records, including minutes of meetings and registers of shareholders. A separate business bank account isn’t just a suggestion for a limited company; it’s a legal necessity because the company’s money isn’t yours until it’s extracted via salary or dividends. For sole traders, keeping personal and business finances separate is best practice to avoid confusion during an HMRC tax investigation. Thankfully, modern cloud accounting software removes the manual slog from these tasks. With real-time information, you can see your financial health with just a click of your finger, which relieves you of the complication often associated with business growth.

HMRC and Companies House Requirements

Deadlines are the heartbeat of business compliance. Sole traders must meet the 31 January Self-Assessment deadline, but company directors juggle multiple dates. You usually have nine months and one day after your financial year-end to pay Corporation Tax, and nine months to file accounts. Failing to meet these can result in automatic penalties starting at £150 for late accounts, which can escalate quickly. As your “Diligent Guardian,” we monitor these records closely to prevent problems before they arise. Being a director brings legal duties, including the responsibility to act in the company’s best interest and ensure all filings are accurate and timely.

Making Tax Digital (MTD) in 2026

The digital landscape changed significantly on 6 April 2026. If you’re a sole trader with an income over £50,000, you’re now legally required to follow Making Tax Digital for Income Tax Self-Assessment (ITSA) rules. This means keeping digital records and sending quarterly updates to HMRC instead of just one annual return. Using cloud-based systems like Xero or QuickBooks isn’t just about efficiency anymore; it’s about compliance. These tools allow us to provide real-time information, ensuring you never feel overwhelmed by the transition. We help you move from uncertainty to clarity, allowing you to focus solely and truly on your goals whilst we handle the technical details.

Pros and Cons: A Side-by-Side Comparison

Are you struggling to decide which path will best support your long-term success? Choosing between a sole trader vs limited company structure involves more than just comparing tax rates. It’s about aligning your business model with your personal risk tolerance and future goals. While the sole trader route offers total privacy and minimal setup costs, it leaves you exposed to unlimited personal liability. Conversely, a limited company acts as a reliable shield for your personal assets, though it requires you to manage more complex administration and accept that your financial summaries will be a matter of public record at Companies House. Many business owners overlook the “lost opportunity” cost of staying as a sole trader for too long, missing out on thousands in potential tax savings as their profits flourish beyond the £50,000 mark.

The choice often boils down to a simple trade-off between simplicity and protection. To help you move from uncertainty to clarity, consider these core differences:

- Sole Trader Pros: Absolute privacy, lower accountancy fees, and the ability to keep all post-tax profits.

- Sole Trader Cons: You are personally responsible for all business debts, and you have fewer options for detailed tax planning.

- Limited Company Pros: Limited liability protection, a more professional image for corporate contracts, and flexible profit extraction.

- Limited Company Cons: Higher setup costs, including the £100 digital incorporation fee, and stricter filing deadlines.

Which Structure Suits Your Growth Ambitions?

Do you plan to hire employees or stay as a one-person operation? If your goal is to scale and eventually seek external investment, a limited company is almost always a requirement. Investors rarely put capital into a sole proprietorship because they need a share-based structure to secure their stake. While the sole trader status is ideal for low-risk, lifestyle-focused businesses, the introduction of Making Tax Digital for ITSA on 6 April 2026 means that even “simple” businesses now face quarterly digital reporting. If you’re already handling that level of digital compliance, the leap to a limited company’s administrative framework feels much smaller.

Financial Flexibility and Exit Strategies

A limited company offers a distinct advantage when it’s time to move on. Because it’s a separate legal entity, it’s far easier to sell or pass on to a family member than a sole trader business. You also gain the ability to “roll up” profits within the company, deferring personal tax by keeping funds in the business for future reinvestment or a rainy day. We help our clients look beyond the books to ensure their structure matches their five-year plan. If you’re ready to protect your future, you can book a consultation to discuss your company formation and find the perfect fit for your potential.

How Season Associates Simplifies Your Choice

Are you feeling overwhelmed by the technicalities of the sole trader vs limited company debate? At Season Associates, we believe that accounting should act as a catalyst for your personal freedom rather than a source of constant anxiety. Our “beyond the books” approach means we don’t just crunch numbers; we act as a proactive partner in your success. We provide the calm competence needed to shield you from HMRC complications, offering fixed-fee monthly retainers that cover all your limited company compliance. This transparency ensures you never face an unexpected bill, allowing you to focus solely and truly on your goals whilst we handle the heavy lifting.

We understand that the transition from one structure to another is a significant milestone. Whether you are starting fresh or scaling an existing venture, we relieve you of all the complications associated with statutory filings and tax planning. Our team handles company formations with just a click of your finger, managing everything from the initial Companies House registration to setting up your payroll services. By positioning ourselves as a reliable shield against fines, we ensure your business journey is defined by growth rather than red tape.

Our Tech-Savvy Mentorship

We pride ourselves on being your tech-savvy mentor in an increasingly digital world. With Making Tax Digital for ITSA now a reality for those earning over £50,000 as of 6 April 2026, cloud accounting software implementation is no longer optional. We specialise in Xero and QuickBooks, providing you with real-time information that helps prevent the common errors contributing to the 18.5% tax gap reported by HMRC. By monitoring records closely, we identify potential issues before they escalate into a full HMRC tax investigation. We invite you to a consultation to find your personal tax-efficient sweet spot, ensuring your financial structure is perfectly aligned with your current earnings.

Transitioning from Sole Trader to Limited Company

If your profits have flourished beyond the £50,000 threshold, the move to a limited company can offer significant protection and flexibility. We manage the incorporation process seamlessly, taking care of the £100 digital incorporation fee and ensuring your new entity is set up correctly from day one. Our “no hidden charges” policy for statutory filings and year-end accounts provides the budget certainty every contemporary business owner needs. As your “Diligent Guardian,” we stand between you and the stresses of HMRC regulations, providing the steady support you need to accomplish your long-term potential.

Secure Your Financial Future Today

Deciding on a sole trader vs limited company structure is a pivotal step that shapes your business’s trajectory. You’ve seen that whilst the sole trader path offers agile simplicity, the limited company structure provides a vital shield for your personal assets and more flexible ways to manage your profit. With the 6 April 2026 introduction of MTD for ITSA, the administrative gap is narrowing, making professional guidance a non-negotiable asset for long-term success.

We are here to help your business flourish. Season Associates offers expert tax planning to minimise your HMRC liabilities and transparent, fixed-fee monthly accounting with no hidden charges. As tech-savvy mentors for Xero and QuickBooks, we ensure you always have real-time information at your fingertips. Book a free consultation with Season Associates to find your most tax-efficient structure. You don’t have to navigate these complexities alone. It’s time to focus solely on your goals and watch your potential truly accomplish great things.

Frequently Asked Questions

Is it cheaper to be a sole trader or a limited company?

Operating as a sole trader is generally cheaper because you avoid Companies House filing fees and typically pay lower accountancy costs. However, once your profits reach the £30,000 to £50,000 range, a limited company structure often becomes the more cost-effective choice due to tax-saving opportunities. While the initial setup is more expensive, the long-term tax efficiency can far outweigh the higher administrative overheads. We help you identify this tipping point to ensure you don’t pay a penny more than necessary.

Can I change from a sole trader to a limited company later?

Yes, you can incorporate your business at any time as your venture grows. This process involves registering a new entity with Companies House and transferring your existing business assets and contracts. Many entrepreneurs choose to make this switch when their annual profits exceed the £50,000 Small Profits Rate threshold to benefit from the 19% Corporation Tax rate. We manage this entire incorporation process for you with just a click of your finger, ensuring a seamless transition.

Do I need a separate bank account as a sole trader?

While it isn’t a legal requirement for sole traders, having a separate bank account is highly recommended to keep your personal and business finances distinct. Clear separation makes it much easier to monitor your records closely and provides a transparent trail if you ever face an HMRC tax investigation. For a limited company, a separate business account is a legal necessity. This is because the company is a separate legal person and its funds must be handled entirely independently from your personal cash.

What is the “dividend tax” and how does it work in 2026?

Dividend tax is the tax you pay on profits you extract from your company after it has already paid Corporation Tax. For the 2026/27 tax year, you have a small Dividend Allowance of £500, which means the first £500 of dividends are tax-free. Beyond this, you’ll pay 10.75% if you’re a basic rate taxpayer or 35.75% if you’re in the higher rate bracket. This remains a popular way to pay yourself because dividends don’t attract National Insurance contributions, unlike a standard salary.

Can a limited company have only one person?

Yes, you can be the sole director and sole shareholder of a limited company. This is a very common structure for contractors and consultants who want the professional prestige of a “Ltd” suffix without the need for a large team. You retain total control over every decision whilst enjoying the protection of limited liability. This setup ensures your personal home and assets are shielded from business debts, providing the peace of mind you need to focus truly on your goals.

How much does an accountant cost for a limited company vs a sole trader?

Accountancy fees for a limited company are usually higher because the sole trader vs limited company administrative requirements differ significantly. A company requires statutory accounts, a Corporation Tax return, and a Confirmation Statement, whereas a sole trader only needs a Self-Assessment return. We provide transparent, fixed-fee monthly retainers with no hidden charges for both structures. Our tech-savvy mentors ensure you receive real-time information and expert support, regardless of which path you choose to follow.

What happens if I forget to file my accounts with Companies House?

Failing to file your accounts on time leads to automatic financial penalties that increase the longer you wait. For a private limited company, the fine is £150 if you’re up to one month late, rising to £1,500 if you’re more than six months overdue. These penalties double if you miss the deadline two years in a row. We act as your Diligent Guardian, monitoring your filing deadlines closely to ensure you never face these unnecessary costs or the stress of compliance failures.

Does being a limited company make it easier to get a mortgage?

Not necessarily, as most lenders focus on your sustainable income rather than your specific business structure. When comparing a sole trader vs limited company application, lenders look at net profit for sole traders and a combination of salary and dividends for directors. Since 2026, many lenders also consider retained profits within a company as part of your affordability. Providing three years of accurate, real-time records from your cloud accounting software is the best way to prove your reliability to a lender.

https://shorturl.fm/hcshj

https://shorturl.fm/h7G53

https://shorturl.fm/edMLB