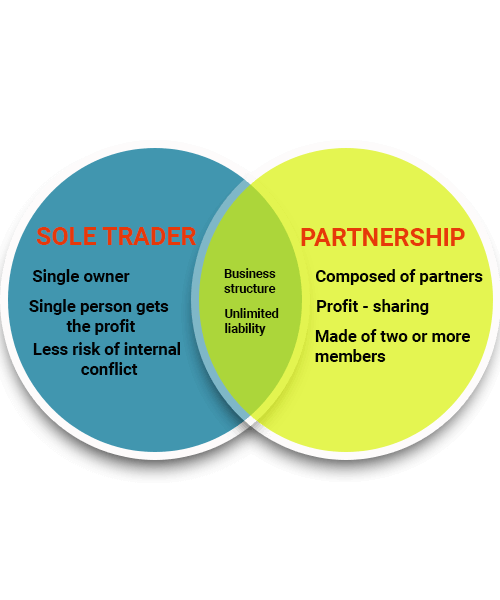

Sole Trader and Partnership

A business can be set up in innumerable ways. Two such types of business set ups are Sole Trading and Partnerships.

Sole Trader and Partnership

Sole Trading is the one of the simplest form of business set up, where a business is managed and owned by a single person. He is the owner of the business and is responsible for all affairs of the company. The sole trader has unlimited liability and is responsible for all the affairs of the company including but not limited to debts, profits, tax etc.

Partnership on the other hand involves at least two individuals who come together to manage and own a business. They too have unlimited liability, however, the profits and losses in such a set up are shared between partners. In partnership, each partner is taxed on their individual profit.

Advantages of being a Sole Trader or a Partner are:

- Easy to start the business with less formalities

- Responsibility of managing and ownership lies with one or less number of individuals.

- Control is in the hand of the owner completely

- Affairs of the business can be kept confidential

- Cost of running the business is less compared to other forms of set up

- Less administrative expenses

Why Choose Us

We, at Season Associate, provide a wide range of services to assist you build up a sole trading or partnership firm. There are several aspects which one should consider while starting up a business.

Although, being a sole trader or opening a partnership firm are simple forms of setting up a business, there are numerous processes that are required to be followed and regulations which have to be complied with. We provide assistance to our clients with personalised advice on each of the following:

Common Mistakes made by Sole trader and Partnership Firms

Although these two forms of business have very limited exposure to manpower and help maintain privacy and confidentiality of the business, there are few mistakes which the owners commonly make. Here are few such mistakes which the owners should avoid for a smooth and long lasting venture:

- Common Mistakes made by Sole trader and Partnership Firms

- Reconciliation of incomings and outgoings of finances should be done on a regular basis to ensure smooth functioning.

- One should maintain receipts of all the transactions including the ones done at a personal level to expand the business such as meeting expenses.

- Accounting of taxes should not be left for last minute payment and adjustment in the books of accounts.

- The owners should keep themselves aware of the existing rules, regulations governing their business and amendments in the same in due course.

- IT infrastructure should be updated constantly in regular intervals.

Get a Quick Enquiry

For availing our services and getting a professional advice on your tax returns at a fixed and comparative price connect with our executives now.

Difference between Sole Trader and Partnership

Every individual, before starting up a business, gives a thought to start a business on his own or to share the idea and related liabilities with others. The decision for this depends on each person’s expectation from the business, the comfort level he has with the operation of the business model and the laws and legislation regulating the type of set up. To understand this further and arrive at a decision of which kind of set up should one opt for, one should understand the difference between the two forms.

We have listed below few differences between a Sole Trader and Partnership firm:

- Sole Trader

- Entire risk of the business is dependent on one person.

- Only one person can create this set up and hence there is no requirement of any agreement.

-

A sole trader is not dependent on any other person for decision making.

. - This set-up does not require any legal formalities to be done before starting the business.

- Partnership

- Risk of the business is shared among members as per the partnership deal agreement.

- Minimum number of members required to start a partnership are 2 and hence an agreement is mandatory.

- A sole trader is not dependent on any other person for decision making. Decision has to be made in consensus with all the partners.

- This set-up does not require any legal formalities to be done before starting the business. Few legal formalities have to be done and it is regulated by Partnership Act 1932.

Frequently Asked Questions

Each business has its own advantages and disadvantages. While sole trading has complete control of one person who is the owner, partnership is less risky and expensive. Thus, it depends on the person’s outlook of the set up and his capability to bear the risk.

Sole trader accounting requires maintenance of proper records of all financial transactions. The owner should maintain a statement of profit and loss and prepare balance sheet for the account. Sole trader accounting also provides for audits to be done for tax purpose.

Sole trading is the easiest form of business to close. Since sole trading is not governed by any legislation, the owner can wind up whenever he wants. The only thing which the owner has to settle before closure of business are the accounts including but not limited to liabilities, if any.

Partnership firms on the other hand are governed by an agreement and hence the dissolution would be on the basis of terms of the agreement.

Quick Links

Contact info

- Season Associates, 12 Coleman Road, Dagenham, RM9 6JU

- info@seasonassociates.co.uk

- 07789 038 444 / 02079932090