Who Needs to Do Self-Assessment? The 2026 Guide to UK Tax Returns

That nagging question, “Do I need to do a tax return?” can cause a surprising amount of stress. Perhaps your side-hustle has started to grow, you’ve begun renting out a property, or your salary has crossed a new threshold. Suddenly, the familiar world of PAYE tax feels a long way away, and the thought of an HMRC letter can be daunting.

You are not alone. Each year, over 12 million people in the UK navigate this very system, and with significant digital changes on the horizon for 2026, clarity has never been more important. This guide is designed to give you a definitive answer. We will walk you through exactly who needs to do Self-Assessment, demystify the key triggers, and show you how to approach the process with calm competence, not confusion.

Who needs to do Self-Assessment? The core criteria for 2026

At its heart, Self-Assessment is the system HMRC uses to collect Income Tax that hasn’t been automatically deducted from wages or pensions. If all your income is taxed at source through Pay As You Earn (PAYE), you generally don’t need to worry. However, several common scenarios will require you to register and file a return.

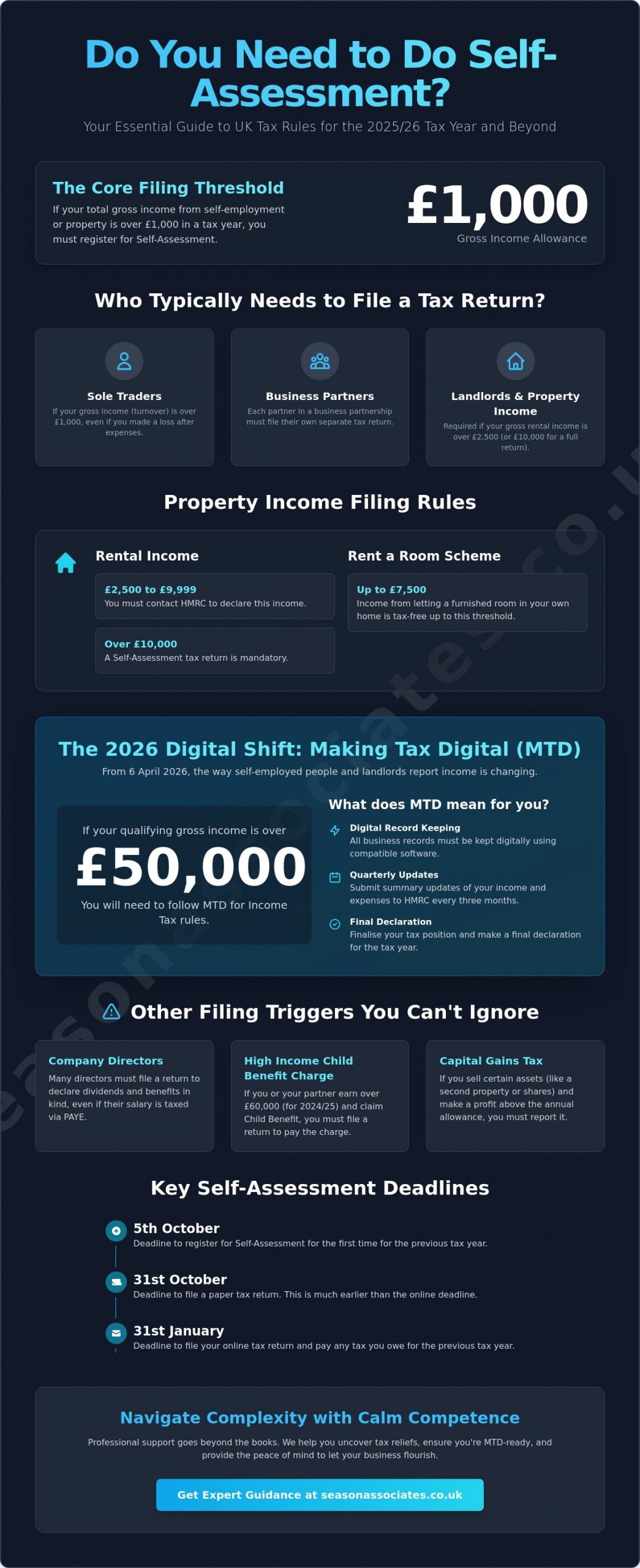

- Sole Traders: The most common group required to file are the self-employed. If you are a sole trader with a gross income (your total earnings before taking off any expenses) of more than £1,000 in a tax year, you must file a Self-Assessment tax return.

- Business Partners: If you are a partner in a business partnership, you must register and file a personal tax return, declaring your share of the profits.

- Untaxed Income: This includes income from abroad that you need to pay UK tax on, or other untaxed earnings from savings, dividends, or investments that exceed your personal allowances.

It’s a common misconception that having a PAYE job makes you exempt. Whilst most employees remain outside the system, specific triggers, which we’ll explore below, can pull you in. The key is to understand all your income streams, not just your primary salary. (Making Tax Digital shift)

The £1,000 Trading Allowance explained

The Trading Allowance is a tax exemption for up to £1,000 of income from self-employment, casual jobs, or selling goods. It’s crucial to understand this applies to your gross income (turnover), not your profit. This distinction is where many people get caught out.

Practical Example: Let’s say you started a small business selling custom prints on Vinted. Your total sales for the year were £1,300. The cost of your materials and postage was £500, so your profit was £800. Because your gross income of £1,300 is over the £1,000 threshold, you must register for Self-Assessment and declare it, even though your profit is below the allowance.

Interestingly, some people with an income below £1,000 still choose to file a return. This is often to make voluntary Class 2 National Insurance contributions, which count towards your State Pension entitlement.

Property income and landlords

Receiving income from property is another primary trigger for Self-Assessment. Landlords have a similar £1,000 property allowance on gross rental income. However, the rules become stricter as your income grows:

- If your gross rental income is between £1,000 and £2,500, you must contact HMRC.

- If your gross rental income is over £2,500, you are required to file a Self-Assessment tax return.

Those using the government’s Rent a Room scheme can earn up to £7,500 tax-free from a lodger. If you earn more than this, you must complete a tax return. It’s also important to note that from 2026, many landlords will need to keep digital records and provide updates to HMRC as part of the Making Tax Digital transition.

Directors, high earners, and the 2026 Making Tax Digital shift

Your role at work or your salary level can also be a deciding factor. Being a company director or a high earner often comes with an automatic requirement to file, as your tax affairs are typically more complex than a standard PAYE employee.

- Company Directors: It’s a common requirement for company directors to file a tax return. This is because you may receive income from various sources, such as dividends, which need to be declared to ensure the correct amount of tax is paid.

- Making Tax Digital (MTD): From April 2026, a major change is coming. If your total qualifying income from self-employment or property is over £50,000, you will be mandated to follow MTD for Income Tax rules.

- Quarterly Updates: This MTD shift moves away from a single annual filing. Instead, you’ll need to use compatible software to keep digital records and send quarterly updates of your income and expenses to HMRC, followed by a final declaration. As Tech-Savvy Mentors, we help our clients navigate this digital transition smoothly.

Directors and Dividend Income

If you are a director of your own limited company, you likely pay yourself a combination of a small salary and dividends. Whilst there is a tax-free dividend allowance (£500 for the 2024/25 tax year), any income above this must be declared on your Self-Assessment return. This allows HMRC to see your total earnings and apply the correct tax bands, ensuring you remain compliant and avoid any unwelcome surprises. This is where detailed tax planning becomes invaluable, helping you structure your remuneration in the most efficient way. (official government guidance)

The £150,000 threshold and high-income earners

Previously, anyone earning over £100,000 was automatically required to file a tax return. HMRC recently raised this threshold to £150,000. However, even if you earn between £100,000 and £150,000, you may still need to file to address issues like the tapering of your Personal Allowance.

A tell-tale sign that you might need to file is an unusual tax code, such as ‘OT’, which means you have no tax-free allowance. This can happen if your income is high or if HMRC doesn’t have enough information. You can check your details easily through your HMRC Personal Tax Account. As wages rise, a phenomenon known as “fiscal drag” is pushing more employees into higher tax brackets and, consequently, into the Self-Assessment system for the first time.

The “Hidden Triggers”: Child Benefit and Capital Gains

Beyond self-employment and high earnings, there are several “hidden triggers” that catch thousands of people off guard every year. These often relate to family circumstances or one-off financial events and can result in an unexpected requirement to file a tax return.

- High Income Child Benefit Charge (HICBC): This is one of the most common surprises. If you or your partner have an individual income over £60,000 and one of you claims Child Benefit, you must file a return to repay some or all of it.

- Capital Gains Tax (CGT): Selling certain assets for a profit can trigger a tax liability. If the gain is above your annual tax-free allowance, it must be reported via Self-Assessment.

- Savings Interest: If you earn interest from savings or investments that exceeds your Personal Savings Allowance and isn’t taxed at source, you’ll need to declare it.

With the right professional support, these triggers can be managed as routine financial health checks rather than sources of stress.

High Income Child Benefit Charge (HICBC)

The HICBC is a frequent and confusing trap. For the 2024/25 tax year (which you report on by January 2026), the charge applies if one partner in a household has an adjusted net income of over £60,000. Crucially, the responsibility to file a tax return and pay the charge falls on the highest earner, regardless of who actually receives the benefit payments. A recent government report highlighted that thousands of families have been hit with backdated fines for failing to declare this, making it vital to monitor your records closely.

Selling assets and Capital Gains

Capital Gains Tax is due on the profit you make when you ‘dispose of’ an asset that has increased in value. Common assets that trigger a Self-Assessment return include:

- A property that is not your main home (e.g., a buy-to-let or holiday home)

- Shares or investments not held in an ISA or PEP

- Crypto-assets like Bitcoin

- Business assets

The “annual exempt amount” is the amount of profit you can make each tax year before CGT is due (£3,000 for 2024/25). It’s also vital to know that for UK residential property sales, you have a separate 60-day window to report and pay the estimated tax, which runs alongside your main Self-Assessment duty.

Key dates and preparing your 2025/26 records

Knowing the deadlines is half the battle. For the 2025/26 tax year (which runs from 6 April 2025 to 5 April 2026), the key dates are non-negotiable. Starting early fosters a sense of calm competence and avoids the last-minute January rush.

- 5 October 2026: The deadline to register for Self-Assessment for the first time.

- 31 October 2026: The deadline for submitting a paper tax return.

- 31 January 2027: The final deadline for online Self-Assessment submissions and for paying any tax you owe.

For a complete overview of all important deadlines, you can read our complete guide to essential tax return dates.

Organising your paperwork “with a click”

Modern accounting is about real-time clarity, not a shoebox full of receipts. Using cloud-based software like Xero or QuickBooks allows you to track income and expenses as they happen, making tax time far less stressful. Key documents you’ll need to gather include:

- Your P60 (if employed) and any P11D for benefits in kind.

- Records of self-employed income and expenses.

- Statements of interest from banks and building societies.

- Details of any pension contributions.

At Season Associates, we help clients implement these digital tools, making the process of filing “beyond the books” feel truly effortless.

The cost of missing the deadline

HMRC’s penalty system is strict and automated. Missing the 31 January deadline by just one day results in an immediate £100 penalty. The costs then escalate significantly with daily penalties, interest on unpaid tax, and further fines after 3, 6, and 12 months. In the last tax year, nearly one million people filed late. These penalties create unnecessary business stress and can easily be avoided. Investing in professional help, with transparent, fixed fees and no hidden charges, is often far cheaper than falling foul of the penalty regime.

Why professional support offers more than just compliance

You can, of course, follow the “DIY” approach to your tax return. But for many, this creates more questions than answers. The alternative is the “Diligent Guardian” model of a professional accountant. We don’t just fill in boxes; we identify tax reliefs and allowances you might otherwise overlook, ensuring you pay the right amount of tax, and not a penny more.

The real value is the peace of mind that comes from knowing your relationship with HMRC is being calmly and correctly managed. This allows you to focus solely and truly on your goals, whether that’s growing your business, planning for the future, or simply enjoying your life.

Beyond the books: Strategic tax planning

A one-off tax return only shows a snapshot in time. We believe in looking at the whole picture. As a Tech-Savvy Mentor, we help you prepare for upcoming changes like Making Tax Digital and plan for future tax efficiency. Our fixed-fee monthly retainers are designed to provide this year-round support, ensuring you are always compliant and in control, without any surprise bills. It’s about building a resilient financial foundation for your future.

Your next steps to financial clarity

Take a moment to review your income streams. Are you a sole trader earning over £1,000? A landlord? A high earner claiming Child Benefit? If the answer to any of these is yes, or if you’re simply unsure, it’s time to seek clarity. Think of us as your reliable shield against HMRC complications, here to provide the answers you need.

Relieve the complication and speak to Season Associates today.

https://shorturl.fm/4WNzR

https://shorturl.fm/AN6gA